In this article

- There is no universally best savings vehicle for retirement. Every tool solves a different problem. The question is whether the problem you need solved matches what the tool was designed to do.

- CDs and annuities both protect your principal, but they are built for different jobs. A CD is a short-term savings instrument. An annuity is a long-term contract that can generate guaranteed lifetime income, something a CD cannot do.

- Staying fully invested in the market during retirement is not automatically the right move. The sequence in which your returns arrive matters as much as the average return, and drawing withdrawals from a falling account creates math that is genuinely hard to recover from.

- Variable annuities are a separate category. The concerns about fees you may have read about often apply specifically to them, not to fixed or indexed annuities. Understanding that difference matters before you decide.

The Honest Framing: There Is No Universally Best Option

Here's the thing most financial comparisons get wrong. They frame the question as "annuity vs. CD" or "annuity vs. the market" as if one has to win and one has to lose. But that's not how any of this actually works near retirement. These tools aren't competing for the same job. They're solving different problems.

A CD solves one problem: safe short-term storage of cash with a predictable rate. The market solves a different problem: long-term growth when you have the time and the risk tolerance to absorb volatility. An annuity solves yet another set of problems: protecting principal from market losses, generating income you cannot outlive, or both. None of these is universally better. Each one is right for what it is designed to do.

So the honest framing isn't "which is best." It's "which risks do you actually need protection from right now, and which tool was built to solve that?" That's the question worth thinking through, and it's what this page is designed to help you do. If you want to start with the basics first, the full annuity overview covers what an annuity actually is before we compare it to anything else.

Annuity vs. CD: Where Each One Protects You, and Where Each Falls Short

CDs and annuities are the most common comparison we hear, and it makes sense why. Both protect your principal. Both have a contract term. Both involve handing your money to a financial institution and getting a predictable return. But the similarities end there, and the differences matter more than most people realize before they choose one.

Better for Money You Need Soon

Where a CD Wins

- FDIC-insured up to coverage limits (an annuity is not FDIC-backed)

- Great for short-term parking, 1 to 3 years, with a known maturity date

- Simple: no contract complexity and no rider choices to make

Better for Long-Term Income

Where an Annuity Wins

- Can guarantee income for life, which a CD cannot. See generating income

- Interest grows tax-deferred in a non-qualified account

- Covers more ground for money held 5+ years and later turned into income

The liquidity trade-off is worth naming directly. CDs have early withdrawal penalties, and so do annuities. Annuity surrender periods typically run longer, 5 to 10 years, though most contracts allow 10% annual free withdrawals during the term. If access to the full amount within 2 years is a real possibility, a CD is the more appropriate tool. If you are working with funds you genuinely won't need to touch for several years, the annuity's longer commitment is often justified by what it can do for you in return.

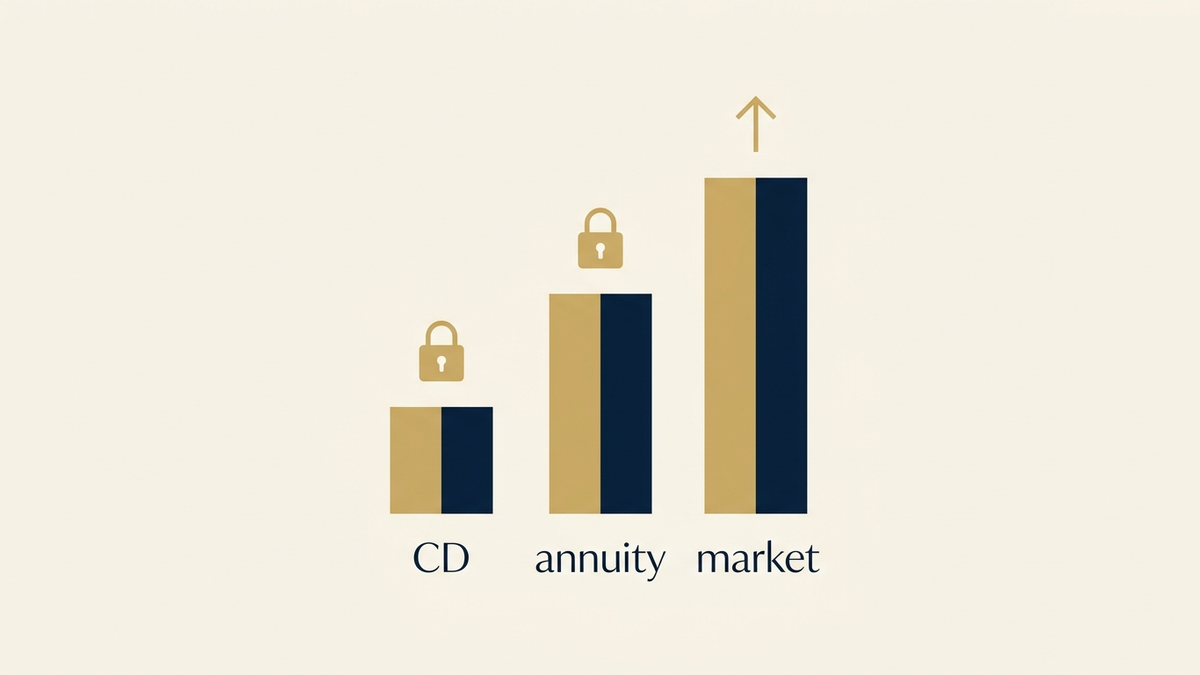

The trade in one picture: CDs and annuities protect your principal, the market offers more growth potential with more risk. Illustrative.

Annuity vs. Leaving It in the Market: the Trade Between Upside and Protection

Staying fully invested in equities through retirement is a strategy that works well for some people. If you have significant guaranteed income from other sources, a long timeline, and a genuine tolerance for watching your account value drop by 30% without changing your withdrawal behavior, then staying in the market may serve you fine. But most people approaching or entering retirement don't fit that description, and there's a specific reason why.

The concept is called sequence-of-returns risk, and it's worth understanding before you decide. Here's the core idea: the order your investment returns come in matters as much as the average return itself. If you retire, start taking withdrawals, and the market drops significantly in your first year or two, you are selling shares at their lowest price to fund your living expenses. That pulls capital out of the recovery. A 30% loss requires roughly a 43% gain just to break even, and you are drawing down the entire time you wait for that recovery. The math is not forgiving.

This is not an argument that equities are wrong for retirement. A diversified approach makes sense for most people, and keeping a portion of your savings in growth-oriented assets is reasonable at almost any age. The real question is whether the portion of your savings you genuinely cannot afford to lose is sitting in the right place. Money you need to live on in the next 5 to 10 years has a different job than money you are growing for 20 years. Treating them the same way is where people get hurt. For a deeper look at protecting savings from sequence-of-returns risk, that page covers the specific tools designed for that job.

A Note on Variable Annuities: Why Fee Layering Tends to Undercut the Benefits

When people come to us having read negative things about annuities, they are usually describing variable annuities, not fixed or indexed ones. That distinction is important, and it's worth being direct about why we generally steer this audience in a different direction.

A variable annuity invests your premium in market-based sub-accounts, which means your principal is exposed to market losses. Unlike a fixed or indexed annuity, there is no contractual floor protecting you from a bad year. You can lose money. On top of that, variable annuities tend to carry multiple layers of fees: a mortality and expense charge, administrative fees, sub-account management fees, and often additional rider fees if you want income guarantees. When you add those together, the total annual cost can run meaningfully high. And here's the problem with that: those fees reduce your balance every year regardless of how the market performs. When the market is flat or down, you are paying for participation in a return you did not receive.

This is not a blanket statement that variable annuities are never appropriate for anyone. They are contracts, and every situation is different. But for someone approaching retirement who is looking for principal protection and predictable income, the fee structure of a typical variable annuity tends to work against the goals that brought them there in the first place. The products we spend most of our time on, fixed indexed annuities and multi-year guaranteed annuities, are structured differently and solve a different set of problems. If you want a clear picture of what those look like, growing safely covers the mechanics.

How to Choose the Right Tool for Your Situation

There is no formula that produces the right answer automatically. But there are questions worth asking yourself before you commit to any approach. Here's what we think matters most for someone in the 55 to 65 range.

- What is this money actually for? Short-term access needs, long-term growth, and lifetime income are three different jobs. The right tool depends entirely on which one applies to the money you are looking at.

- What would a 30% market drop do to your retirement plans? If the honest answer is "it would materially change things," then some portion of your savings has a job that market exposure cannot safely do. That's not a flaw in your plan, it's a signal about where protection belongs.

- Do you have guaranteed income beyond Social Security? A pension or other guaranteed income stream changes the calculus. If your essential expenses are covered, the portion of your savings in equities is doing a different job than the money you actually need.

- How long can you realistically commit to leaving this money in place? Annuities work best for money you will not need to access in full for 5 or more years. If your timeline is shorter, a CD or liquid savings vehicle is more appropriate.

- What keeps you up at night? Outliving your money is a real risk. Running out of income in year 20 of retirement is not an abstract concern. If that fear resonates, an income-generating annuity is solving a real problem, not adding unnecessary complexity.

- Are you looking at the right kind of annuity? The objections you may have heard, high fees, principal at risk, lack of transparency, tend to apply to a specific product type. If you are thinking about a fixed or indexed annuity and the concerns you have are based on reading about variable products, it's worth separating those conversations. A specialist can help you understand the difference without any commitment required.

Who This Guidance Fits, and Who It Does Not

Honest education means being clear about both sides. The comparison on this page is most useful for a specific type of person. If you are outside that description, some of these trade-offs land differently.

This tends to be most relevant if you

- Are between 55 and 65 and actively thinking about how to structure your savings for retirement. The decisions you make in this window have an outsized effect on how retirement actually goes.

- Have a meaningful lump sum, often an IRA, 401(k) rollover, or inheritance, that is currently sitting in cash, low-yield accounts, or a portfolio you feel is mismatched to your actual risk tolerance right now.

- Want to understand how an annuity compares to what you already have before you decide anything. You're not looking for a sales pitch. You want the real comparison.

- Have a specific concern: running out of income, losing too much in a market crash right before or after retirement, or protecting a spouse who may outlive you. Those are problems with specific solutions worth knowing about. See generating income for the income piece.

This probably applies less if you

- Are early in your career with a 20 or 30 year horizon ahead. The protection layer that annuities provide matters most in the years closest to and just after retirement. Early accumulators are generally better served by market-based vehicles for the bulk of their savings.

- Have all of your essential retirement income covered by Social Security, a pension, and other guaranteed sources. If the income question is already answered, the trade-offs shift considerably.

- Need your entire savings to remain fully accessible at any moment. Annuities are contracts with terms. If full liquidity is a hard requirement, a CD or brokerage account is the more appropriate vehicle, and a specialist will tell you that plainly.

If you are not sure where you fall, a 15-minute call is genuinely enough to find out. No commitment, no pressure. Here's how that conversation works.

Common questions about annuities vs. the alternatives

Is an annuity better than a CD?

It depends entirely on what you need the money to do. A CD is better for short-term savings you will need within 1 to 3 years, money you want FDIC insurance on, and situations where simplicity and full liquidity at the end of the term are the priority.

An annuity is better for savings you plan to hold for 5 or more years, for money you eventually want to convert to guaranteed lifetime income, and for non-qualified accounts where tax-deferred growth provides a meaningful advantage. A CD rate resets at maturity to whatever the market offers at that time. An annuity locks in its terms for the contract period and can do things a CD structurally cannot, like pay you a monthly income for the rest of your life. They are different tools. The better question is which one matches the job you actually need done.

Should I just keep my money in the market?

For some people in some situations, yes. If you have significant guaranteed income from other sources, a long time horizon, and a genuine tolerance for volatility, staying invested in equities makes sense for part or all of your savings.

But near retirement, the math changes in an important way. Sequence-of-returns risk means a large loss in your first years of withdrawal can do permanent damage to your retirement balance, because you are selling shares at their lowest price to fund withdrawals. You don't have 20 years to wait for a recovery. The question isn't whether equities are good, it's whether the portion of your savings you need in the next 5 to 10 years can afford the risk of a significant drop. For that portion, a different tool usually serves you better.

Are variable annuities ever a good idea?

Variable annuities are not categorically bad, but they are a different product with a different risk profile and a different fee structure than fixed or indexed annuities. For someone approaching retirement who wants principal protection and predictable income, variable annuities generally work against those goals: your account can decline in a market downturn, and the layered fees reduce your balance every year regardless of performance.

There are situations where a variable annuity might make sense, particularly for someone with a longer time horizon who wants market participation inside a tax-deferred wrapper and is comfortable with the fees. But for most people in the 55 to 65 range who come to us asking about protection and income, fixed and indexed products are more aligned with what they actually need. If you have questions about a specific product, a specialist can walk you through how the fees and risk profile compare without any pressure to commit to anything.

How much of my savings should be in an annuity?

There is no universal answer, and anyone who gives you a specific number without understanding your full situation is guessing. What we can say is that annuities are generally most valuable for the portion of your savings that has a specific job: providing guaranteed income, protecting against sequence-of-returns risk, or both. Most people don't put everything into an annuity, and shouldn't. You still want liquid savings, market exposure for long-term growth, and flexibility.

The right allocation depends on your income gap, meaning the difference between your guaranteed income from Social Security and pensions versus your actual expenses, your health and longevity expectations, and how much market volatility you can genuinely absorb without it affecting your retirement plans. A 15-minute conversation with a specialist is designed to answer exactly this question for your specific numbers. That's what the call is for.

What about bonds? Are they a better alternative to annuities for income?

Bonds and bond funds are a legitimate part of many retirement portfolios. But they solve a different problem than annuities, and they carry their own risks worth knowing about.

Bond funds in particular do not guarantee a specific income stream. Their distributions fluctuate with interest rates and market conditions. When rates rise, bond prices fall, meaning the underlying value of your bond fund drops. There is no contractual floor, no guarantee of principal return, and no lifetime income guarantee. An annuity with a lifetime income rider, by contrast, commits in writing to a payment amount for as long as you live. The guarantees rest on the insurance company's financial strength rather than the bond market, but the predictability of the income stream is categorically different. For generating a reliable, predictable income in retirement, the annuity structure generally outperforms bond funds on that specific dimension.