In this article

- An annuity can work like a personal pension: you hand the insurance company a lump sum and they contractually commit to paying you income for the rest of your life, no matter how long that turns out to be.

- There are two main paths to guaranteed income. You can start receiving payments right away (immediate income via a SPIA), or you can let savings grow first and turn income on later (income riders with a guaranteed lifetime withdrawal benefit on a fixed indexed annuity).

- How much income you receive depends on your age, when you start, whether you need to cover a spouse, and the interest rate environment at the time you set it up. These inputs move the number significantly.

- This is not the right tool if you need full liquidity at any time. The trade-off for a guaranteed income floor is giving the insurance company some control over how the underlying money is structured.

The Core Idea: Your Savings as a Paycheck

Most people retire with a pool of savings and a question they can't fully answer: will it last? Markets move. Lifespans are unpredictable. Taking withdrawals from a portfolio that can drop 20 or 30 percent in a bad year creates real math problems, because you're selling shares at the worst possible time to fund your living expenses.

An income annuity solves a specific part of that problem. You move a portion of your savings into a contract with an insurance company. In return, they commit in writing to paying you a set income for the rest of your life. If you live to 95, the payments keep coming. The insurance company, not you, takes on the longevity risk. That shift is the whole point. It's not about chasing returns. It's about replacing uncertainty with a floor you can count on. See our broader guide to what an annuity is if you want the full picture first.

30+ yrs

A retirement that starts at 62 can run into your 90s. Your income has to last that long.

$0

Reduction to a guaranteed income payment from a market loss once the income is turned on.

Lifetime

How long contractually guaranteed payments continue, no matter how long you live.

Illustrative, for education only. Not a quoted rate, return, or guarantee.

The Main Ways to Get Guaranteed Income

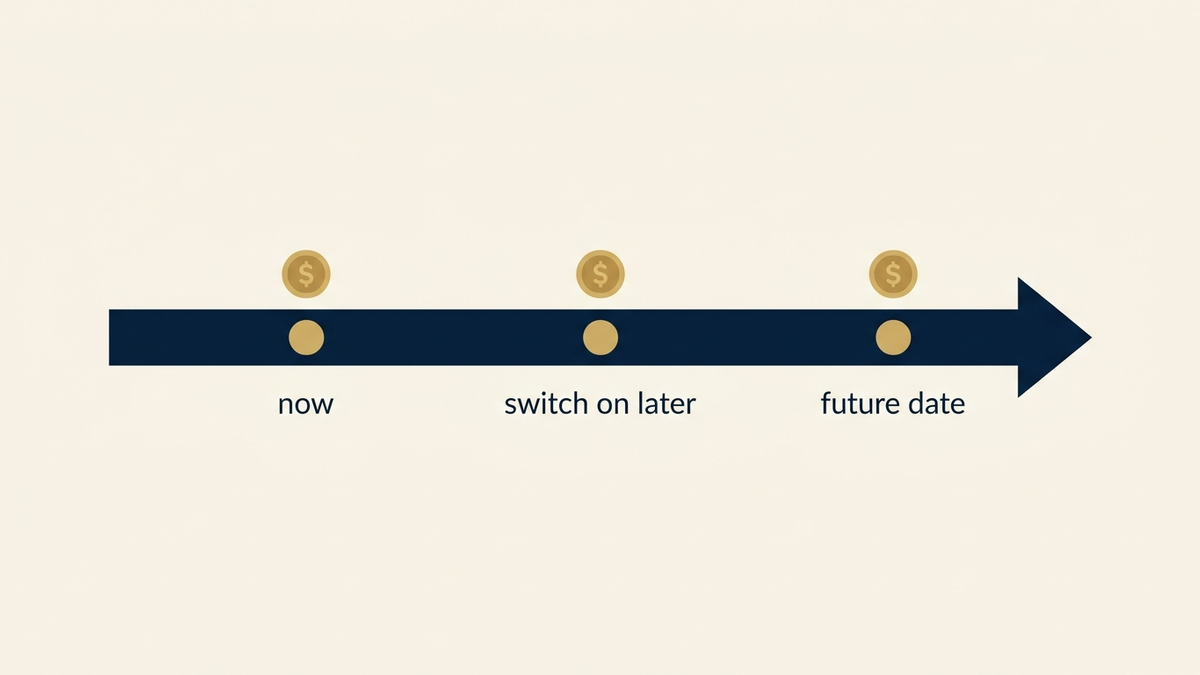

There are two primary approaches to generating lifetime income from an annuity. They solve slightly different problems depending on where you are in retirement.

The main difference is when the income starts: right now, when you flip it on later, or at a set future date. Illustrative.

Immediate Income (SPIA)

A Single Premium Immediate Annuity converts a lump sum into a monthly payment that starts within 30 days. There is no accumulation phase, no account value to track, and no decisions to make later. You hand the insurance company a premium today and start receiving a guaranteed check immediately. This works well for people at or past retirement age who need income to start now. The trade-off is that this is a one-way door: once you set it up, the principal is committed to funding your income stream. Most contracts let you choose payment options that protect a surviving spouse or guarantee a minimum payout period to your estate, but those choices affect the payment amount.

Future Income You Switch On (Income Riders / GLWB)

A Guaranteed Lifetime Withdrawal Benefit (GLWB), also called an income rider, works differently. You put money into a fixed indexed annuity today, and the contract credits a guaranteed income base that grows at a contractually set rate during your accumulation years. When you're ready to retire, you flip a switch and start drawing income from that guaranteed base, regardless of what the account's actual market value has done. This is the grow-safely-then-turn-on-income approach. You keep an account value you can still pass to heirs, while receiving income for life. The income rider typically carries a small annual fee deducted from the account value.

Deferred Income (DIA)

A Deferred Income Annuity is similar to a SPIA, but you choose a future start date several years out. Because the insurance company holds your money longer before payments begin, the eventual monthly payment is often higher than what an immediate annuity would pay on the same premium. Some people use a deferred income annuity as a longevity backstop, designed to kick in at age 80 or 85 and cover expenses if they outlive their other assets. You give up access to the money today in exchange for a larger guaranteed payment later.

What Affects How Much Income You Receive

The income figure you receive is not arbitrary. Several inputs drive it, and understanding them helps you set realistic expectations before you run a formal illustration. For a rough starting point, you can try our Income Estimator tool.

- Your age at start. The older you are when income begins, the higher your monthly payment. The insurance company is calculating how long they expect to pay you. A 70-year-old starting income will receive more per month than a 62-year-old on the same premium, because the expected payment period is shorter. For a 65-year-old with a single-life contract, illustrative income on a SPIA or income rider is often in the ballpark of 5 to 7 percent of the premium per year. That range is illustrative and will shift with interest rates and specific contract terms. It is not a quoted rate or a guarantee.

- When you defer. On income riders specifically, every additional year you wait to turn income on typically increases the guaranteed income base. Deferring from 60 to 65 can meaningfully increase your monthly payment compared to activating income right away.

- Single versus joint life. If you want income to continue for a surviving spouse after you pass, the monthly payment will be lower than a single-life contract. How much lower depends on the age difference between spouses and the specific contract design. For most married couples, joint-life coverage is worth the trade-off.

- Interest rates at the time of purchase. Income annuity payouts are influenced by prevailing interest rates. When rates are higher, the same premium buys more monthly income. This is why comparing illustrations at different points in time can produce very different numbers.

- The contract type and carrier. Payout rates vary by carrier and contract design. An independent review of multiple options, rather than a single illustration from one company, is worth doing before committing. No specific carrier or product is recommended here.

How Annuity Income Fits with Social Security and Pensions

Most people approaching retirement already have some guaranteed income in place, or will have it soon. Social Security is the most common. A pension is less common today, but some people still have one. The question is not whether you need an annuity instead of Social Security. The question is whether your guaranteed income floor is large enough to cover your essential expenses reliably.

Here's how to think about it. Add up your non-negotiable monthly expenses: housing, healthcare, food, utilities. Then look at what Social Security and any pension will cover. If the gap between what you need and what you have guaranteed is meaningful, that gap is exactly what an income annuity is designed to fill. The goal is to put a floor under your fixed expenses so that market volatility only affects your discretionary spending, not whether you can pay your bills.

People who already have a large pension covering most of their expenses often have less need for an income annuity. People with smaller Social Security benefits, no pension, and a significant portion of retirement savings in a 401(k) or IRA are often the best fit. That savings pool is where income riders and immediate annuities typically come from, often funded by a rollover. See our full comparison of annuities versus the alternatives for a side-by-side look at how different tools stack up.

One practical note on Social Security timing: delaying Social Security to age 70 increases your monthly benefit significantly. Some people use an income annuity as a bridging income stream between ages 62 and 70, letting Social Security grow in the background. That can be a rational strategy, though the right approach depends on health, other assets, and family circumstances.

Who This Fits, and Who It Does Not

Honest education means being direct about both sides. An income annuity is a powerful tool for the right situation. For the wrong situation, it creates problems.

This tends to fit people who

- Are at or near retirement, roughly ages 58 to 72, and need to convert accumulated savings into reliable monthly income.

- Have a meaningful gap between their guaranteed income (Social Security, pension) and their fixed monthly expenses.

- Are worried about running out of money if they live longer than expected. A 65-year-old today has a meaningful probability of living into their mid-to-late 80s.

- Want to protect a spouse who may outlive them. A joint-life income contract continues payments to a surviving spouse regardless of what happens to the market.

- Have savings in a 401(k) or IRA they are not sure how to draw down efficiently without sequence-of-returns risk eroding the balance in bad markets.

This is probably not the right fit if you

- Need your entire savings pool to remain fully liquid. Income annuities involve committing capital to a contract. That is not a hidden trap. It is the feature: you're trading flexibility for certainty. But if full access at any moment is essential, this is not the right vehicle for that money.

- Have all of your essential expenses already covered by Social Security and a pension. Adding an annuity income layer on top of a fully covered expense base does not solve a problem you have.

- Are significantly under 55 and have decades of compounding ahead. The math on lifetime income is most powerful when it's working over a shorter, later horizon.

- Have significant health concerns that meaningfully reduce expected lifespan. Lifetime income annuities are most valuable when you live a long time. Shorter life expectancies change the calculus, and that is worth a direct conversation with a specialist before committing.

If you're not sure which side of this you're on, a 15-minute call is designed exactly for that conversation. No commitment, no pressure.

Common questions about annuity income

How much income will my savings produce?

The honest answer is: it depends on your age, the type of contract, current interest rates, and whether you need joint-life coverage. As a conceptual starting point, a 65-year-old with a single-life income contract can often illustrate income in the range of 5 to 7 percent of the premium per year. On a $200,000 premium, that is roughly $10,000 to $14,000 per year. These are illustrative ranges, not quoted product rates or contractual guarantees. The actual number from a formal illustration will depend on the specific product and carrier at the time of purchase.

The best way to get a real number is to run an illustration. Our Income Estimator gives you a rough starting point, and a specialist can walk you through a formal illustration based on your actual situation.

What happens to the money if I die early?

It depends on the contract type and the options you selected when you set it up. For a SPIA, you can typically choose a period-certain option that guarantees payments for a minimum number of years. If you pass away before that period ends, the remaining payments go to your named beneficiary. A return-of-premium death benefit is available on some products, ensuring the insurance company pays out at least as much as you put in.

For income riders on fixed indexed annuities, your beneficiary typically receives the remaining account value. The income base used to calculate your payments and the actual account value are different numbers, and your heirs receive the account value, not the income base. Understanding that distinction before you sign is important.

The short version: the fear that "the insurance company keeps everything" does not reflect how most modern income products work. But the specific rules vary by contract, and a specialist can walk you through exactly what your beneficiary would receive under any contract you're considering.

Can I still access my money after setting up annuity income?

It depends on the product type. A SPIA is the most restrictive: once you exchange the premium for an income stream, that money is committed. You cannot withdraw it as a lump sum. Some SPIA contracts include a cash refund or lump-sum option at certain points, but these are not standard features.

An income rider on a fixed indexed annuity is more flexible. You have an account value that you can withdraw from, subject to surrender period rules and any free-withdrawal provisions, which are typically 10 percent per year during the contract term. Turning on the income rider does not eliminate your access to the account. It layers a guaranteed income floor on top of it.

If having access to your full principal at any point is a firm requirement, a SPIA is probably not the right vehicle. An income rider gives you more flexibility while still providing the lifetime income guarantee.

Is the income guaranteed for life, or does it stop at some point?

For both SPIAs and income riders with a lifetime income feature, the payments are contractually guaranteed for as long as you live. That is the defining feature of a lifetime income annuity. The insurance company cannot stop payments because you've outlived their actuarial expectation, because your account value has dropped to zero, or because market conditions change.

The guarantee is backed by the financial strength of the insurance company itself, not the FDIC. This is why carrier financial strength matters and why working with someone who has reviewed multiple carriers is worth more than taking the first offer you see. State guaranty associations provide limited backstop coverage if a carrier becomes insolvent, but the primary protection is the carrier's own financial strength.

When should I start income from my annuity?

For SPIAs, the question is simple: when do you need the income? Most people use them at or near retirement, when they need cash flow to replace a paycheck.

For income riders on fixed indexed annuities, there is often a meaningful incentive to wait. The guaranteed income base grows at a contractually specified rate during deferral, often 5 to 8 percent per year on the income base (not the account value). Waiting even a few extra years can meaningfully increase your guaranteed monthly payment. That said, there is a point of diminishing returns, and the right decision depends on your cash flow needs, your other income sources, and how long you plan to defer.

As a general framing: if you have other income sources that can cover your expenses for a few more years, deferring income on a rider contract often produces a materially better outcome. If you need income now, a SPIA or immediate activation of your rider is the right call. A specialist can run both scenarios side by side so you can see the actual numbers before deciding.