In this article

- The biggest financial danger in the years just before and after retirement is not earning too little. It is losing too much at the wrong time and not having enough runway to recover.

- Two annuity types are designed specifically for protected growth: Fixed Indexed Annuities (FIAs), which link your growth to a market index with a guaranteed floor of zero, and MYGAs, which work like a CD with a fixed guaranteed rate for a set term.

- Both tools have real trade-offs. FIAs cap or limit how much of the index's gain you capture. MYGAs lock in a rate but don't offer market participation. Honest education means knowing both sides.

- Neither of these tools is right for every dollar you have saved. They are designed for a specific job: protecting the money you cannot afford to lose while still earning something meaningful on it.

The Problem This Solves

Here's the thing most people don't hear until it's too late. The market risk you take at 45 is very different from the market risk you take at 62. When you're 45, a bad year is frustrating. You have 20 years to let compound growth fix it. When you're 62, a bad year can be genuinely damaging in a way that takes years to work through, if you have the time to work through it at all.

The concept is called sequence-of-returns risk, and it basically means this: the order that your investment returns come in matters as much as the average return itself. If you retire and start taking withdrawals, and the market drops 30% in your first two years, you are selling shares at their lowest price to fund your living expenses. That pulls money out of the recovery. The math is not forgiving. A 30% loss requires a roughly 43% gain just to get back to where you started, and you're drawing down the whole time.

This is the problem that protected-growth tools are built to solve. You are not trying to maximize your returns at this stage. You are trying to protect what you have built so that one bad market cycle doesn't force you to start over. The goal is simple: protect the principal, capture some growth, sleep at night.

The Two Main Tools for Protected Growth

When people come to us asking about growing savings safely, two tools come up again and again. They are different from each other in important ways, and the right choice depends on what you specifically need. Both are annuity products, both are contracts with an insurance company, and both protect your principal. That's where the similarities end.

Growth Linked to a Market Index

Fixed Indexed Annuity (FIA)

- Growth follows a market index, up to a cap or participation rate

- Principal protected: zero in a down year, never a loss

- Typically 5 to 10 year terms, often 10% annual free withdrawals

- Can add an income rider for a guaranteed paycheck later. See generating income

A Fixed Rate, Like a CD

Multi-Year Guaranteed Annuity (MYGA)

- Fixed guaranteed rate for the full term, no market exposure

- Recent multi-year terms have broadly ranged 4 to 6 percent (illustrative, not a quote)

- Interest grows tax-deferred, unlike a bank CD

- Usually 3 to 7 year terms; renew, roll, or cash out at the end

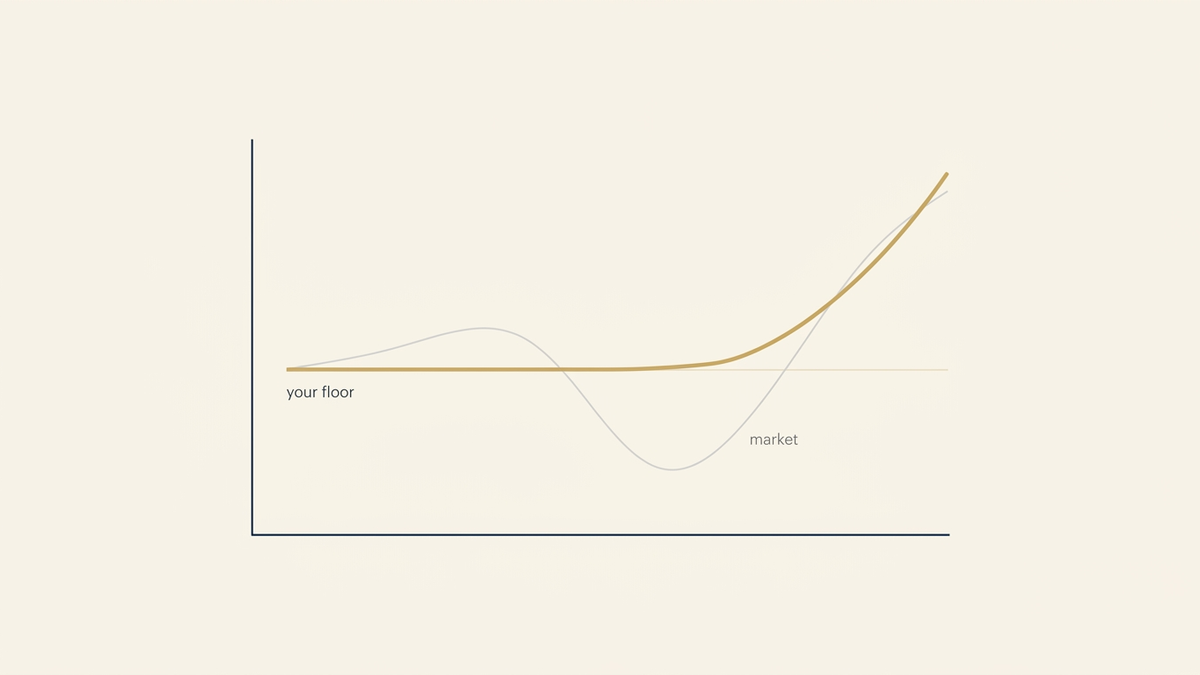

How the floor works: in a down year your balance holds while the market drops, then you share in the recovery. Illustrative.

How to Think About Caps, Participation Rates, and the Floor

If you are considering an FIA, you will run into three terms that describe how your growth is calculated. They are worth understanding at a conceptual level before you look at any specific contract.

- The floor. This is the most important feature. The floor is a contractual guarantee that your account value will not go below zero due to market losses. In a year when the index your contract is linked to loses 20%, your account earns zero for that year, not negative 20. Your principal is protected. You won't find a 0% floor in a brokerage account or a mutual fund. It is a feature specific to this contract type.

- The cap. A cap is the maximum interest rate your account can earn in a given period, regardless of how well the index performs. If your contract has a 10% annual cap and the index returns 18% that year, you earn 10%, not 18%. The insurance company keeps the difference. This is part of how they fund the floor guarantee. The cap is the cost of the protection, and it's a real cost worth understanding before you sign.

- The participation rate. Some contracts use a participation rate instead of, or in addition to, a cap. A participation rate means you earn a set percentage of whatever the index returns. If your participation rate is 60% and the index returns 12%, you earn 7.2%. Again, the insurance company retains the rest to fund the floor guarantee and their operations.

- Spreads. Some contracts use a spread as a third lever. A spread is a fixed percentage that gets subtracted from the index return before your credit is calculated. If the index returns 10% and your contract has a 2% spread, you earn 8%. Different contracts use different combinations of these three levers. They all accomplish the same basic thing: defining how you share in the upside with the insurance company in exchange for them taking on the downside risk.

The honest framing here is this: you are not getting market returns. You are getting a portion of market-linked growth with a guaranteed floor. That trade-off is valuable in a specific situation. It's not a magic product, and anyone who presents it as one is not giving you the full picture. See common annuity myths for a realistic look at what these products can and cannot do.

Annuity vs. Leaving It in the Bank or the Market

There is no universally "best" place to keep savings near retirement. The right answer depends entirely on what you need the money to do. Here is an honest comparison of the three most common options.

Leaving it in a bank CD or savings account

A bank CD is FDIC-insured, simple, and safe. If you need full flexibility, are parking money for a short period, or want the simplest possible option, a CD is a reasonable choice. The limitations are also clear: rates tend to be modest, especially for shorter terms, and the rate resets at maturity to whatever the market is offering at that time. For someone 60 years old with money they won't touch for several years, a MYGA will often offer a higher rate than a comparable bank CD with comparable safety, and the growth is tax-deferred rather than taxable in the year it's earned. The trade-off is that a MYGA is not FDIC-insured. The guarantee rests on the insurance company's financial strength, with a backstop from state guaranty associations. See our full comparison of annuities vs. the alternatives for a deeper look at how these tools stack up.

Leaving it in the market

Staying fully invested in equities through retirement is a strategy that works well for some people, particularly those with stable income from other sources, a long timeline, and a high tolerance for volatility. The problem for most people approaching retirement is not that equities are bad. It's that the sequence-of-returns math described above becomes genuinely dangerous when you're drawing withdrawals from an account that can drop significantly in value. Taking 4% per year from a balance that drops 30% in your first year of retirement is a very different outcome than taking 4% from a balance that simply earns nothing for a year. One shrinks your base in a way that's hard to come back from. The other just means a flat year.

This is not an argument against keeping any money in the market. Most financial planners would tell you a diversified approach makes sense for most people. The question is how much of your savings can afford to take a big hit right now, and whether the portion that cannot afford it is sitting in the wrong place.

Who This Fits, and Who It Does Not

Honest education means being direct about both sides. A protected-growth annuity is a specific tool that solves a specific problem. For the right situation, it's genuinely valuable. For the wrong situation, it creates unnecessary friction.

This tends to fit people who

- Are within 5 to 15 years of retirement and have savings they cannot afford to lose to a market downturn. If a 30% drop right now would materially change your retirement plans, that money deserves protection.

- Have a lump sum, often from an IRA or 401(k) rollover, sitting in cash or a low-yield account that isn't growing meaningfully. A MYGA or FIA can put that money to work safely while you figure out the next step.

- Want their savings to grow during the accumulation years and then eventually convert to guaranteed income at retirement. FIAs can be paired with income riders to do exactly that. See how annuities generate retirement income for the full picture.

- Are worried about starting over after a crash. The fear of getting sequence-of-returns risk wrong is real and it's worth solving with the right tool rather than hoping the timing works out.

This is probably not the right fit if you

- Are in your 30s or 40s with a long investment horizon ahead of you. The floor protection matters most near retirement. Early in your accumulation years, you have time to ride out market cycles, and equities will likely outperform the capped growth of an FIA over a long enough period.

- Need your entire savings to remain fully liquid at any moment. Both FIAs and MYGAs have surrender periods during which early withdrawals above the free-withdrawal provision can trigger a charge. If full access at any time is a firm requirement, these contracts are not the right vehicle for that money.

- Have all your essential retirement expenses covered by Social Security, a pension, or other guaranteed income, and have no meaningful risk of a market downturn changing your lifestyle. Adding a protected-growth layer on top of an already secure plan may not move the needle for you.

- Are looking for maximum growth potential. These tools give up some upside in exchange for downside protection. If your goal is to maximize returns and you can absorb the volatility, a market-based approach may serve you better for that portion of your savings.

If you are not sure which side of this you are on, a 15-minute call with a specialist can give you a clear answer. No commitment, no pressure, just honest clarity on whether one of these tools belongs in your plan. Read our guide on whether an annuity is right for you if you want to think it through first.

Common questions about growing safely

Can I lose money in a fixed indexed annuity?

You cannot lose money in a fixed indexed annuity due to market performance. That is the defining feature of the 0% floor. If the index your contract tracks has a bad year and drops 25%, your account earns zero for that year rather than declining by 25%. Your principal stays intact.

There are two important caveats. First, if you withdraw more than your contract's free-withdrawal provision before the surrender period ends, you may incur a surrender charge. Second, some FIA contracts have optional riders (like income riders) that carry a small annual fee, typically deducted from the account value. That fee can reduce your balance slightly over time even in a flat or low-growth year. The floor protects against market losses, not against fees. Understanding the full fee structure of any contract you are considering is worth doing before you commit.

How is a MYGA different from a CD?

They are more similar than they are different, which is why MYGAs are often described as the annuity world's version of a CD. Both lock in a fixed rate for a set term. Both protect your principal. Both have penalties for early withdrawal.

The differences worth knowing: A CD is FDIC-insured by your bank. A MYGA is issued by an insurance company and backed by the carrier's financial strength, with limited backstop coverage from state guaranty associations rather than the FDIC. In exchange for that difference in backing, MYGAs have typically offered higher rates than comparable bank CDs for the same term, particularly in higher interest-rate environments. The other meaningful difference is tax treatment: a MYGA's interest grows tax-deferred, meaning you don't owe taxes on the earnings until you withdraw them. A CD's interest is taxable as ordinary income in the year it's earned. For savings sitting in a non-qualified (non-IRA) account, that deferral can be a real advantage.

What is a cap or participation rate, and why does it exist?

A cap is the maximum interest rate your FIA account can earn in a given crediting period. A participation rate is the percentage of the index's return you receive. Both are mechanisms the insurance company uses to share the upside with you while retaining enough to fund the floor guarantee and their operating costs.

Here's a simple way to think about it. The insurance company is taking on your downside risk, meaning they absorb the loss when the market goes down. In exchange, they keep a portion of your upside when the market goes up. The cap or participation rate is how they define that share. A higher cap or participation rate is better for you, because you keep more of the gain. Caps and participation rates can change at contract renewal, which is one reason reviewing a contract's historical rate adjustments and the carrier's practices matters before you sign.

Is my principal actually protected?

In a fixed indexed annuity, yes. Your account value cannot go below zero due to market performance. This is a contractual guarantee, not a market promise. Even in a year when the index drops 40%, your account earns zero for that year and your principal is intact.

The guarantee is backed by the insurance company's financial strength, not the FDIC. This is an important distinction. The carrier behind your contract matters, and their financial ratings are worth reviewing. State guaranty associations provide limited coverage if a carrier becomes insolvent, but the primary protection is the carrier's own financial health. Working with someone who has reviewed multiple carriers rather than relying on a single illustration is worth doing before committing. The risk is not market loss. It is carrier insolvency, which is rare and partially covered, and the opportunity cost of capped growth versus staying fully in equities.

What happens when the term ends?

At the end of a MYGA term or an FIA's surrender period, you typically have a window of time, often 30 days, during which you can access your money without penalty, renew into a new contract term, or roll the funds into a different product. This window is important to know about, because if you miss it and the contract auto-renews, you may be locked in for another term at the new rate.

For FIAs, the end of the surrender period also means the end of surrender charges. You retain the 10% free-withdrawal provision in most contracts during the term, but full access without any potential charge generally requires waiting for the surrender period to finish. After that point, the money is yours to use, reinvest, or roll to another annuity without penalty. A good specialist will remind you well in advance of any renewal window and walk you through your options at that time.